Fleet safety technology will lead to improved driver behavior and lowered accident rates. Both fleets and fleet insurers would like to see safety technology implemented, but the key question often is who should pay for it? The answer, logically enough, is that the technology should be at least partially funded by the party who receives the value. With virtually all technologies, there is value delivered to both the insurer and the fleet. By understanding the continuum of value delivered by different types of technology, a guide can be established determining which party receives value and finances the solution.

A significant consideration when determining where the value of technology lies is the determination of the amount of the fleet insurance deductible. By understanding deductible coverages, further determination can be made regarding the relative value received by the fleet vs. the insurer.

Today’s insurance market

We are in a “hard market” for insurance now, meaning insurance is harder to get and almost always more expensive than it was in the past. To maintain profitability, fleets are evaluating the need to accept higher fleet insurance deductibles, thus lowering insurance costs or at least minimizing the amount of increase. Insurance companies are more often providing incentives to insured fleets to use safety technology and passing on improved coverage with technology deployments.

Deductible Options

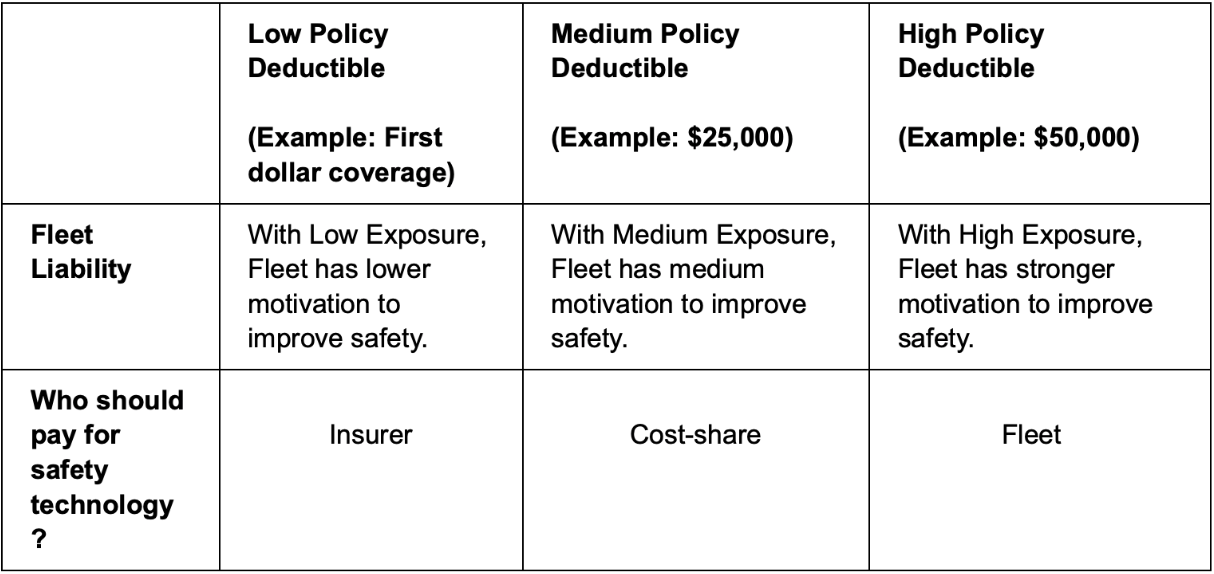

Insured fleets, like consumers, have the option of choosing how much of a deductible is associated with their fleet vehicle insurance coverage. First dollar coverage means the insurer owns all of the liability and the fleet, while paying a higher premium for this level of coverage, has little liability. With first dollar coverage, the fleet has little motivation to invest in technology that helps lower future losses.

On the other hand, a very high fleet insurance deductible means the fleet will be financially responsible for a larger portion of losses related to accidents and claims. Therefore, the fleet will be more motivated to implement technology that will improve loss histories over time. Obviously a higher deductible means more exposure for the fleet. The option of a higher deductible is steadily increasing now because of the choice/need to lower insurance costs.

Motivation for funding fleet technology

In addition to the impact the deductible has on determining the relative value delivered to the fleet vis-a-vis the insurer, there is another important consideration for fleets and insurers to consider. Various technologies deliver different values but the recipient of the majority of that value is determined by exactly what that technology is. Examples of how various technologies benefit fleets and insurers differently are as follows:

Telematics

Telematics, represented by the classic OBD device installed in the vehicle, provides the primary value of operational efficiency to the fleet. Driver and vehicle location can be determined immediately, and devices can communicate with the engine bus–thus enabling operational efficiency. The value of telematics to the fleet is much stronger than the value to the insurer, given that insurers care very little about vehicle location or operational considerations. Marginal improvement in driver behavior can be achieved only with the active and ongoing support of fleet management to notify drivers of safety deficiency, determine corrective actions, and track its impact over time.

Dash Cams

Dash cams record driving incidents and may improve driver behavior, thus improving accident exposure. This technology aids in claim settlements and potentially improves driving behavior, leading to less accidents. Therefore, insurers may be more motivated to see their insured fleets use vehicle cameras. Dash cams deliver more safety value than telematics solutions in that they can identify and correct accident-related behaviors, such as unsafe following distance and poor reactions. They can also assist in driver identification, and identify elements of distraction driving. Value is delivered both to the fleet and the insurer through improved behavior correction as well as the recording of truth. Many insurers are now incentivizing the use of cameras with variable financial participation between the fleet and the insurer.

FNOL

First Notice of Loss (FNOL) benefits the insurer almost exclusively so it becomes the insurer’s job to incentivize the use of such technology. The fleet receives little value in the quick identification of the details of an accident, while the insurer can receive tremendous value by identifying and seeking settlement early on any accident-related issues. It is therefore incumbent upon the insurer to incentivize and potentially co-fund this capability.

Cell Phone Distraction Avoidance

Cell phone distraction avoidance technology will provide protection against liability for cell phone abuse for both the fleet and the insurers. Accidents related to cell phone misuse will commonly result in large adverse settlements. Cell phone distraction avoidance technology is unique in that it is largely “self-correcting”, low cost, and mitigates risk associated with the huge liability of proven cell phone misuse.

Summary

In conclusion, the combination of understanding and potentially using fleet insurance deductibles can be a key determinant of who receives the primary value of mitigating driving risk. The higher the exposure fleets or insurers have in a given accident will logically determine that group’s motivation to invest in technology. The organization receiving significant value from the deployment of technology, may make the determination of more aggressively supporting the deployment.

Finally, it should be understood exactly who receives the value from the different technology solutions available to the fleet. Again, the party receiving value may make the determination to more aggressively incentivize the use of the technology through funding.